Life insurance rates by age

Home – Life insurance rates by age

Lock In Your Lowest Life Insurance Rate Today

At San Diego Life Insurance Center (SDLIC), we help you lock in your lowest premium when you’re young and healthy. Because life insurance rates rise with age, getting coverage now can save you thousands over time—and give your loved ones the protection they deserve.

How Age Affects Life Insurance Rates

Get covered now and lock in today’s low rates

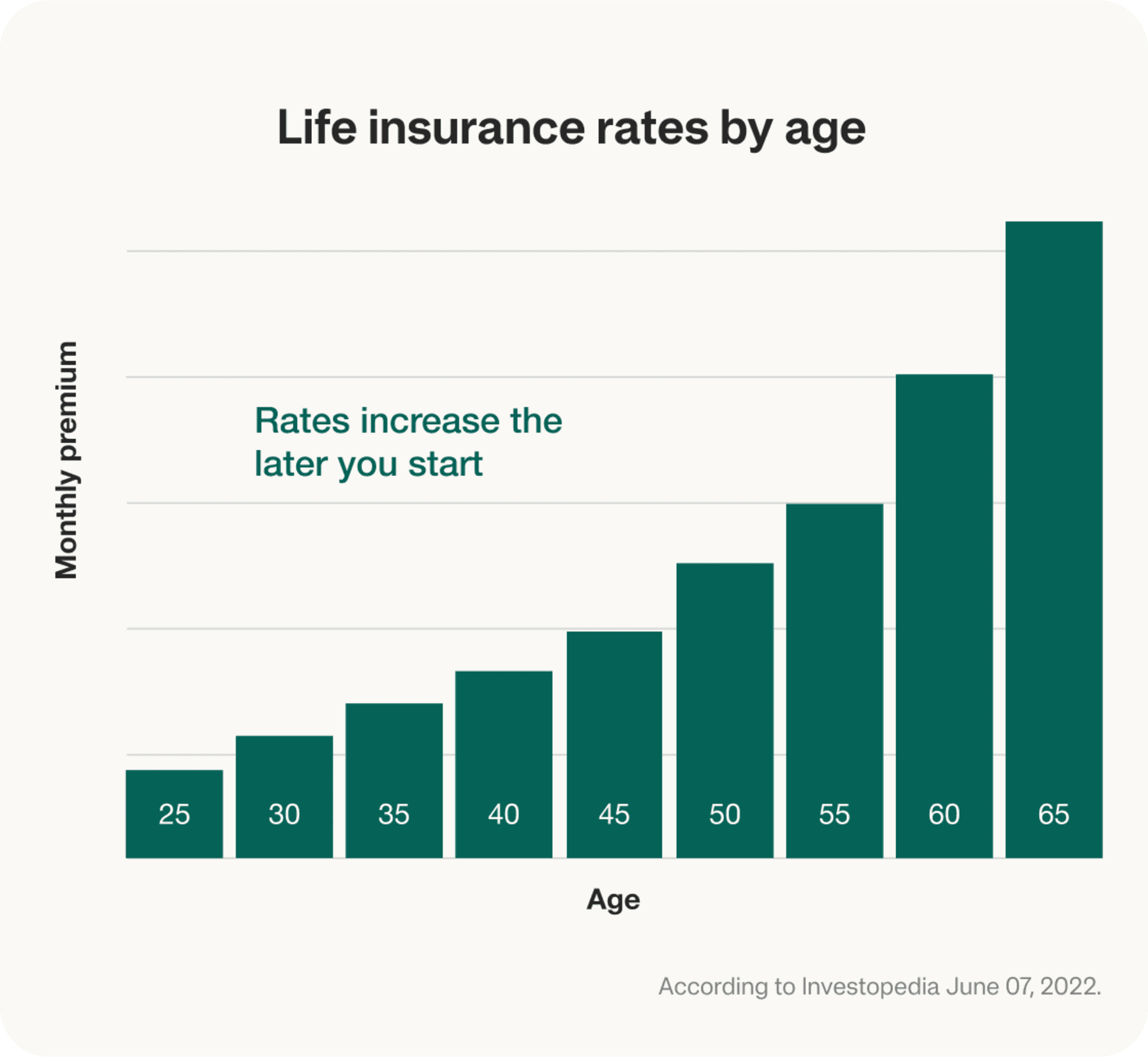

Life insurance premiums increase each year you wait to apply. According to industry data, a healthy 40-year-old non-smoking male could get a 10-year, $1 million term policy for just $54/month. Waiting until 45 could raise the same policy to $73/month—that’s an extra $228 per year.

Locking in your policy now means your rate stays the same for your entire term—no matter how your age or health changes.

Average Term Life Insurance Rates by Age

(10-year term, $1M coverage, non-smoker, good health)

Getting insured earlier doesn’t just lower your monthly cost—it can save you thousands over the life of your policy.

Even if you’re older, term life insurance is often more affordable than permanent insurance, especially if you only need coverage for a set period.

Why Younger People Pay Less

Life insurance is based on risk, and younger people are usually:

Healthier

Less likely to develop serious medical issues

Statistically less likely to pass away during the term

Because of this, insurance companies offer lower rates to younger applicants. This isn’t age discrimination—it’s simply how actuarial data works. Locking in coverage while you’re young helps you secure long-term savings and peace of mind.

Common Mistakes to Avoid

Waiting until you have kids

Even if you don’t have dependents yet, life insurance can cover debts, funeral costs, and income replacement—taking the burden off your partner or family.

Assuming you’ll stay healthy

Life can change quickly. Health conditions like diabetes or cancer can raise premiums—or make you ineligible. Buying early helps protect your future insurability.

Relying only on employer coverage

Workplace plans are usually small (1–2x salary) and disappear if you leave your job. Having your own policy gives you portable protection that stays with you no matter where you work.

How to Get the Best Rates

Here’s how to lower your cost and get approved at the best rate possible:

Maintain good health: Exercise, eat well, and address any existing conditions before applying.

Choose the right coverage: Only buy what you need—extra coverage means extra cost.

Quit smoking: Smokers pay significantly more. Staying smoke-free for 12+ months can cut your premium.

How SDLIC Makes It Easy ?

Choose Your Plan

Pick the right coverage amount and term length with help from our licensed experts or our simple coverage calculator.

Apply in Minutes

Complete our secure online application. Just answer questions about your age, health, and lifestyle—no medical exam required.

Get Covered Fast

Get an instant decision in most cases. Once approved, your coverage can start immediately.